Image: U.S. Home Ownership and Subprime Origination Share

{kind=link}

{kind=link}

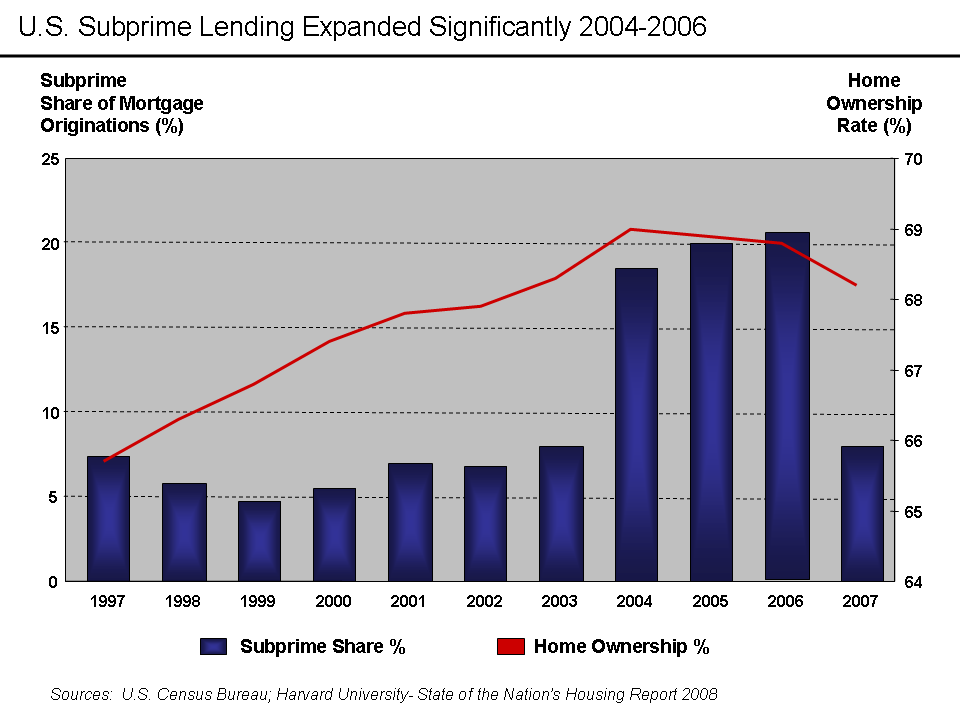

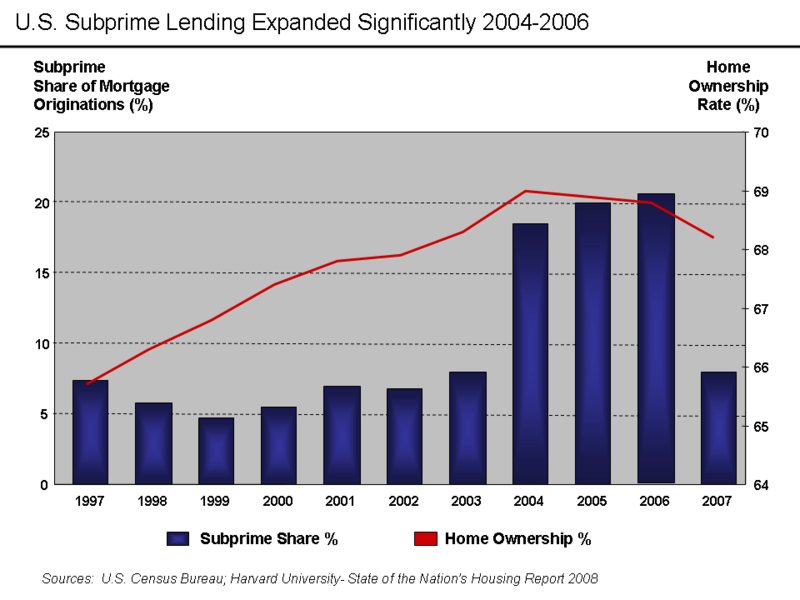

Description: There are various mortgage categories defined based on the credit quality of the borrower. These include subprime, Alt-A, and Prime. The share of subprime mortgages is shown in the diagram. It is the ratio of the dollar value of subprime mortgages to all originations, expressed as a percentage. The level of home ownership is based on the percentage of American households that own homes rather than rent. Subprime mortgages remained below 10% of all mortgage originations until 2004, when they spiked to nearly 20% and remained there through the 2005-2006 peak of the housing bubble.[1] A proximate event to this increase was the April 2004 decision by the SEC to relax the net capital rule, which encouraged the largest five investment banks to dramatically increase their financial leverage and aggressively expand their issuance of mortgage-backed securities. This applied additional competitive pressure to Fannie Mae and Freddie Mac, which further expanded their riskier lending.[2] Excerpts from the Harvard Report: "Subprime mortgages rose from only 8 percent of originations in 2003 to 20 percent in 2005 and 2006, while the interest-only and payment-option share shot up from just 2 percent in 2003 to 20 percent in 2005." "Making matters worse, multiple risks were often layered onto individual loans. For example, large shares of subprime mortgages also had discounted initial rates that reset after two years, leaving borrowers vulnerable to payment shock. In addition, lenders eased underwriting standards, offering loans requiring little or no downpayment or income documentation, and some engaged in behavior viewed as predatory. This meant that many loans were underwritten without a clear measure of the borrowers’ ability to repay and without equity cushions as protection against defaults. "Housing speculators were also readily able to get loans to buy investment properties, relying on soaring house price appreciation to flip the units and resell at a profit." Other interpretations: Home ownership peaked before subprime lending really took off in 2004-2006. Based on this data, subprime loans were not solely responsible for the expanding home ownership rate in the years leading to the crisis, as subprime lending remained a minor portion of the mortgage origination share. Source Data U.S. Census Bureau Harvard 2008 State of Nation's Housing

Title: U.S. Home Ownership and Subprime Origination Share

Credit: Transferred from en.wikipedia to Commons.

Author: Farcaster at English Wikipedia

Usage Terms: Creative Commons Attribution-Share Alike 3.0

License: CC BY-SA 3.0

License Link: http://creativecommons.org/licenses/by-sa/3.0

Attribution Required?: Yes

Image usage

The following 2 pages link to this image:

{kind=link}